Capitalization of Earnings: The Preferred Method for Stable, Mature SMBs

Cashing In on Profits: Understanding the Capitalization of Earnings Method for Small Business Valuation

Ever wondered how investors figure out what a consistently profitable small business is really worth? One of the key tools in their arsenal is the capitalization of earnings method. Think of it like this: if a business consistently generates a certain level of profit each year, how much would you need to invest today at a reasonable rate of return to achieve that same annual income? That's the core idea behind this valuation approach.

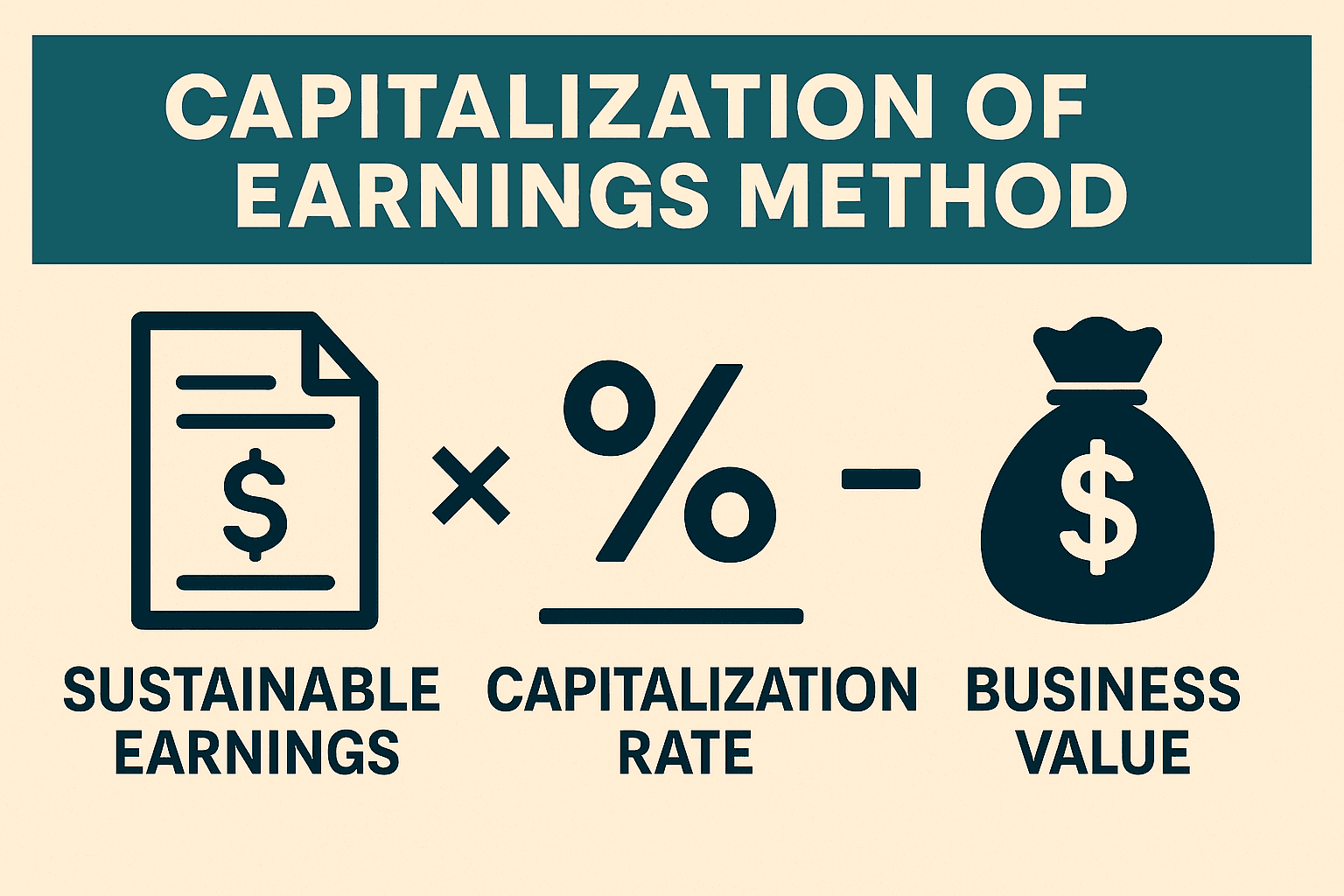

The capitalization of earnings method estimates a business's value based on its sustainable earnings and a chosen capitalization rate. It essentially treats the business as an income-generating asset.

The Core Components: Earnings and the Capitalization Rate

At the heart of this method are two crucial elements:

1. Sustainable Earnings

This isn't just a look at last year's profit. It involves analyzing the business's historical earnings to determine a normalized and representative level of profit that the business is expected to generate consistently in the future. This might involve:

Averaging Profits: Taking an average of profits over the past 3-5 years to smooth out any unusual spikes or dips.

Adjusting for Non-Recurring Items: Removing one-time gains or losses that are unlikely to happen again (e.g., a large insurance settlement or an unusual legal expense).

Considering Owner's Compensation: Adjusting for instances where the owner's salary might be significantly above or below market rates. The goal is to reflect the true earning power of the business, regardless of the owner's specific compensation structure.

Tax Considerations: Using after-tax earnings is often preferred as it represents the actual profit available to the owners.

2. Capitalization Rate (Cap Rate)

This is the rate of return an investor would expect to receive on their investment in this particular business, considering its risk. It's expressed as a percentage. Determining the appropriate cap rate is critical and often involves considering factors such as:

Risk-Free Rate: The return on a very safe investment (like government bonds).

Industry Risk: Some industries are inherently more volatile or competitive than others, requiring a higher return to compensate for the increased risk.

Company-Specific Risk: Factors like the business's size, financial health, management team, customer concentration, and competitive advantages all play a role. A riskier business will typically have a higher cap rate.

Growth Expectations: Businesses with strong growth potential might warrant a slightly lower cap rate, as investors anticipate future increases in earnings.

Market Conditions: Current economic conditions and investor sentiment can influence cap rates.

The Calculation: Turning Earnings into Value

Once you have a reasonable estimate of sustainable earnings and an appropriate capitalization rate, the calculation is simple:

Business Value = Sustainable Earnings / Capitalization Rate

Example

Imagine "The Cozy Cafe" has demonstrated consistent after-tax profits averaging $50,000 per year after making necessary adjustments. After analyzing the risks associated with the cafe industry and this specific business, a capitalization rate of 20% (or 0.20) is deemed appropriate.

Using the capitalization of earnings method:

Business Value = $50,000 / 0.20 = $250,000

This suggests that based on its consistent earnings and the perceived risk, The Cozy Cafe could be valued at around $250,000.

Visualizing the Impact of Cap Rate

The capitalization rate has a significant inverse relationship with the business value. A lower cap rate results in a higher valuation, and vice versa.

As you can see, even a small change in the cap rate can have a substantial impact on the estimated business value.

When is the Capitalization of Earnings Method a Good Fit?

This method is particularly useful for valuing:

Established and Profitable Small Businesses: Businesses with a track record of consistent earnings are ideal candidates.

Businesses in Stable Industries: Where future earnings are more predictable.

Smaller, Privately Held Companies: Where detailed financial projections for more complex methods (like discounted cash flow) might be less reliable or readily available.

Businesses with a Relatively Stable Growth Rate: The basic capitalization of earnings method assumes a relatively constant level of future earnings. While variations exist for incorporating growth, the fundamental approach works best when growth is not the primary value driver.

When the Capitalization of Earnings Method Might Not Be the Best Choice

This method has limitations and might not be suitable for all businesses:

Startups and Early-Stage Companies: These businesses often have little to no profit history or inconsistent earnings, making it difficult to determine sustainable earnings.

High-Growth Companies: The basic capitalization of earnings method doesn't adequately account for significant future earnings growth, potentially undervaluing these businesses. More sophisticated variations that incorporate growth expectations exist but add complexity.

Businesses in Declining Industries: Historical earnings might not be indicative of future performance in a shrinking market.

Businesses with Highly Cyclical or Unpredictable Earnings: If a business's profitability fluctuates wildly from year to year, determining a "sustainable" level becomes challenging.

Businesses with Significant Assets Not Directly Contributing to Earnings: If a company holds substantial non-operating assets (e.g., excess real estate), this method might not fully capture their value. An asset-based approach might be more relevant in such cases.

Businesses with Owner-Dependent Operations: If the business's profitability is heavily reliant on the owner's personal involvement and might not be easily transferable, this risk should be carefully considered in the cap rate.

Charting the Appropriateness

Scenario | Capitalization of Earnings Appropriateness | Why? |

|---|---|---|

A well-established and profitable local bakery | High | Consistent earnings history in a relatively stable industry. |

A rapidly growing tech startup with minimal profit | Low | Lack of consistent earnings and significant future growth potential not adequately captured. |

A cyclical construction company | Low | Earnings fluctuate significantly with economic cycles, making "sustainable earnings" difficult to determine. |

A consulting firm with consistent client base and profits | High | Stable earnings driven by recurring client relationships. |

A retail store in a declining shopping mall | Low | Past earnings may not be indicative of future performance due to changing market conditions. |

The Bottom Line on Capitalizing Earnings

The capitalization of earnings method is a valuable tool for estimating the worth of stable, profitable small businesses. Its simplicity makes it accessible, but the crucial element is determining a realistic sustainable earnings figure and a relevant capitalization rate that accurately reflects the business's risk and market conditions.

While powerful for the right type of business, it's essential to recognize its limitations, especially when dealing with high-growth, early-stage, or highly cyclical companies. In many cases, using the capitalization of earnings method in conjunction with other valuation approaches can provide a more comprehensive and reliable assessment of a small business's value. It's about finding the right tool for the job to get a clear picture of what those consistent profits are truly worth.