Excess Earnings Method: Properly Valuing Professional Practice Goodwill

Sometimes, a profitable small business seems to be worth more than just the sum of its identifiable assets. This "extra" value often comes from intangible factors like a strong brand, loyal customer base, or a skilled workforce. The excess earnings method is a valuation technique that attempts to capture this intangible value by considering the business's earnings above and beyond what a normal return on its tangible assets would suggest.

Think of it this way: if you invested in similar tangible assets elsewhere, what kind of return could you reasonably expect? If this business is generating significantly more profit than that, the "excess" profit might be attributable to its valuable intangible assets. The excess earnings method tries to quantify this extra earning power.

The Steps Involved: Peeling Back the Layers of Value

The excess earnings method typically involves these key steps:

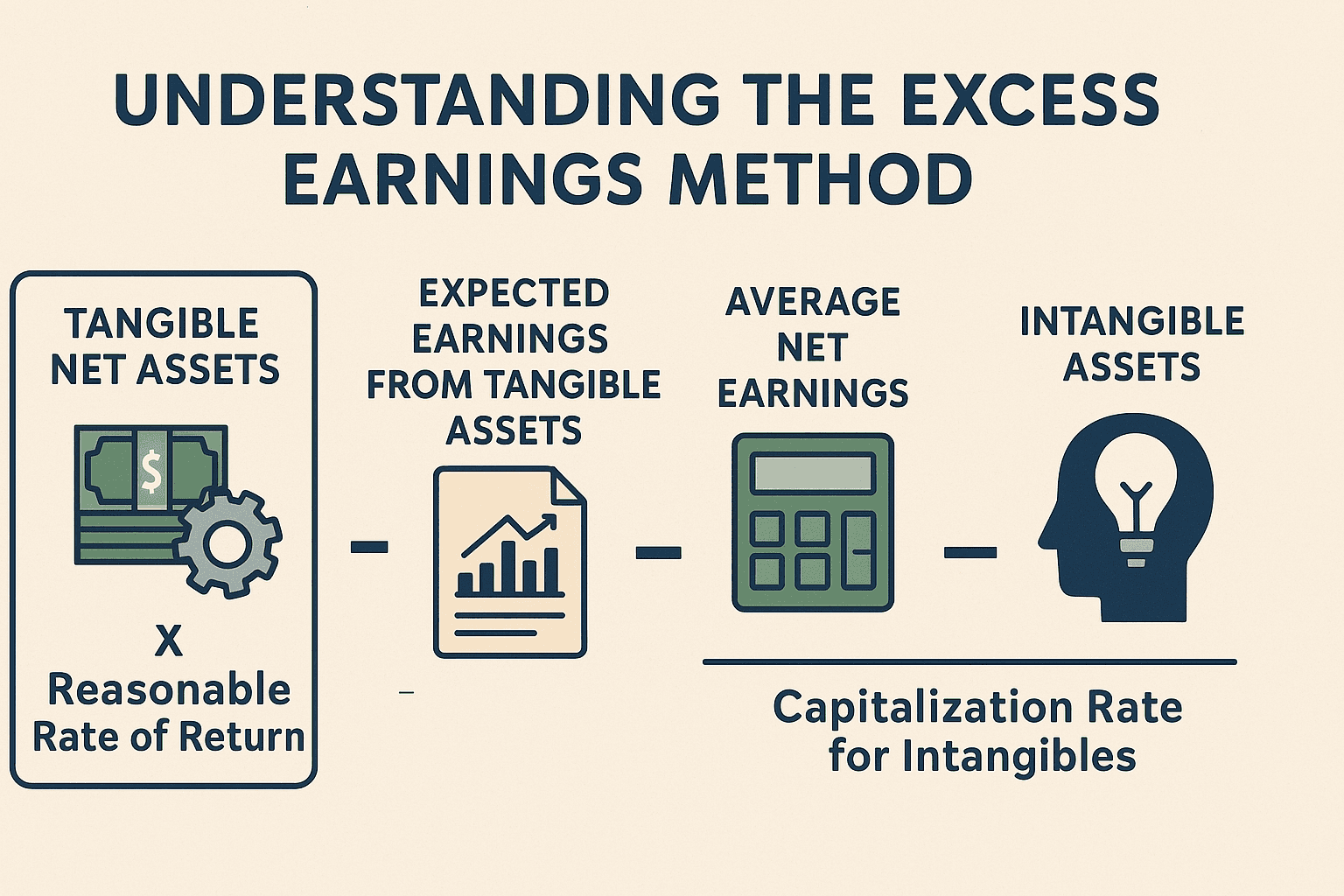

1. Determining the Value of Tangible Net Assets

This is similar to the asset-based valuation method. You identify all the business's tangible assets (cash, accounts receivable, inventory, equipment, real estate) and subtract its total liabilities to arrive at the net tangible asset value. This represents the value of the physical and easily quantifiable resources of the business.

2. Estimating a Reasonable Return on Tangible Assets

You need to determine what a typical rate of return would be for an investment in assets of similar risk and nature. This "reasonable rate of return" is often based on factors like:

Prevailing Interest Rates: The cost of borrowing money.

Risk-Free Rate of Return: The return on very safe investments.

Industry Risk: The inherent risks associated with the specific industry.

Company-Specific Factors: The perceived riskiness of this particular business's tangible assets.

3. Calculating the Expected Earnings from Tangible Assets

Multiply the net tangible asset value by the reasonable rate of return. This gives you the level of earnings that could be expected solely from the tangible assets.

Expected Earnings from Tangible Assets = Net Tangible Asset Value x Reasonable Rate of Return

4. Determining the Average Net Earnings of the Business

Analyze the business's historical earnings (similar to the capitalization of earnings method) to arrive at a normalized and representative level of average net earnings. This should account for non-recurring items and potentially owner's compensation adjustments.

5. Calculating the Excess Earnings

Subtract the expected earnings from tangible assets (step 3) from the average net earnings of the business (step 4). The difference represents the earnings that are attributed to the intangible assets of the business.

Excess Earnings = Average Net Earnings - Expected Earnings from Tangible Assets

6. Capitalizing the Excess Earnings

The excess earnings are then capitalized using an appropriate capitalization rate for intangible assets. This rate is typically higher than the rate used for tangible assets because intangible assets are generally considered riskier and less liquid. Factors influencing this rate include the strength and durability of the intangible assets (e.g., brand reputation, customer loyalty), competitive landscape, and overall market conditions.

Value of Intangible Assets = Excess Earnings / Capitalization Rate for Intangibles

7. Calculating the Total Business Value

Finally, the total estimated value of the business is the sum of the net tangible asset value (step 1) and the value of the intangible assets (step 6).

Total Business Value = Net Tangible Asset Value + Value of Intangible Assets

Illustrative Example: The Local Bookstore

Let's say "Book Nook," a local bookstore, has the following:

Net Tangible Asset Value: $100,000 (including inventory, fixtures, and cash, minus liabilities)

Average Net Earnings: $30,000 per year

Reasonable Rate of Return on Tangible Assets: 10% (0.10)

Capitalization Rate for Intangible Assets: 25% (0.25)

Here's how the excess earnings method would work:

Expected Earnings from Tangible Assets: $100,000 x 0.10 = $10,000

Excess Earnings: $30,000 - $10,000 = $20,000

Value of Intangible Assets: $20,000 / 0.25 = $80,000

Total Business Value: $100,000 (Tangible Assets) + $80,000 (Intangible Assets) = $180,000

In this example, the excess earnings method suggests that Book Nook has $80,000 in value stemming from its intangible assets, likely due to its loyal customer base, good reputation, and prime location.

When is the Excess Earnings Method a Useful Approach?

This method can be particularly helpful in valuing:

Profitable Businesses with Significant Intangible Value: Companies where brand recognition, customer relationships, intellectual property (that isn't formally valued as an asset), or a strong reputation contribute significantly to their earnings.

Established Businesses with a History of Strong Profitability: The method relies on analyzing past earnings to identify the "excess."

Situations Where a Buyer is Willing to Pay for Goodwill: This method explicitly quantifies the value of intangible assets, which is often what buyers are paying a premium for.

When the Excess Earnings Method Might Not Be the Best Fit

Like other valuation methods, the excess earnings method has its limitations:

Difficulty in Determining Appropriate Rates of Return: Selecting the "reasonable rate of return on tangible assets" and the "capitalization rate for intangibles" can be subjective and significantly impact the valuation.

Reliance on Historical Earnings: If past earnings are not indicative of future performance (e.g., due to changing market conditions or loss of key personnel), the method may not be reliable.

May Not Be Suitable for Startups or Unprofitable Businesses: These businesses may not have a track record of consistent earnings to analyze.

Can Be Complex and Subjective: The multiple steps and the need for judgment in selecting rates can make this method more complex than simpler approaches like revenue multiples.

Potential for Double-Counting: Care must be taken to ensure that the "reasonable rate of return" on tangible assets doesn't already implicitly account for some of the business's overall risk, which is then further addressed in the higher capitalization rate for intangibles.

Charting the Appropriateness

Scenario | Excess Earnings Method Appropriateness | Why? |

|---|---|---|

A well-known local restaurant with loyal customers | High | Likely has significant intangible value (brand, reputation, customer base) contributing to earnings beyond its tangible assets. |

A new e-commerce startup with rapid revenue growth but no profit | Low | Lack of consistent historical earnings and the focus on intangible value based on past performance make it unsuitable. |

A manufacturing company with primarily tangible assets | Moderate | Might have some intangible value, but the primary value driver is likely its physical assets. The "excess" earnings might be minimal. |

A business in a rapidly changing technological landscape | Low | Past earnings and the durability of intangible assets may be uncertain. The capitalization rates would be highly speculative. |

A professional services firm with a strong brand and reputation | High | The value lies heavily in its intangible assets (brand, expertise, client relationships) that drive earnings beyond a simple return on physical assets. |

The Final Word on Excess Earnings

The excess earnings method offers a valuable approach to valuing small businesses, particularly those where intangible assets play a significant role in driving profitability. By separating the return on tangible assets from the earnings generated by intangible factors, it provides a more nuanced understanding of the business's overall value.

However, its reliance on subjective rate selection and historical earnings data means it's crucial to apply it thoughtfully and with a thorough understanding of the business and its industry. Often, using the excess earnings method in conjunction with other valuation techniques can provide a more robust and well-supported estimate of a small business's worth, especially when trying to quantify that often elusive "goodwill" factor.