Adjusted Net Asset Method: The Right Valuation Approach for Real Estate Holding Companies

Imagine looking at a company's balance sheet – a snapshot of its assets and liabilities at a specific point in time. The standard balance sheet values assets at their historical cost (what the company originally paid for them), minus depreciation. However, these "book values" might not accurately reflect the current market value of those assets. This is where the adjusted net asset method comes in.

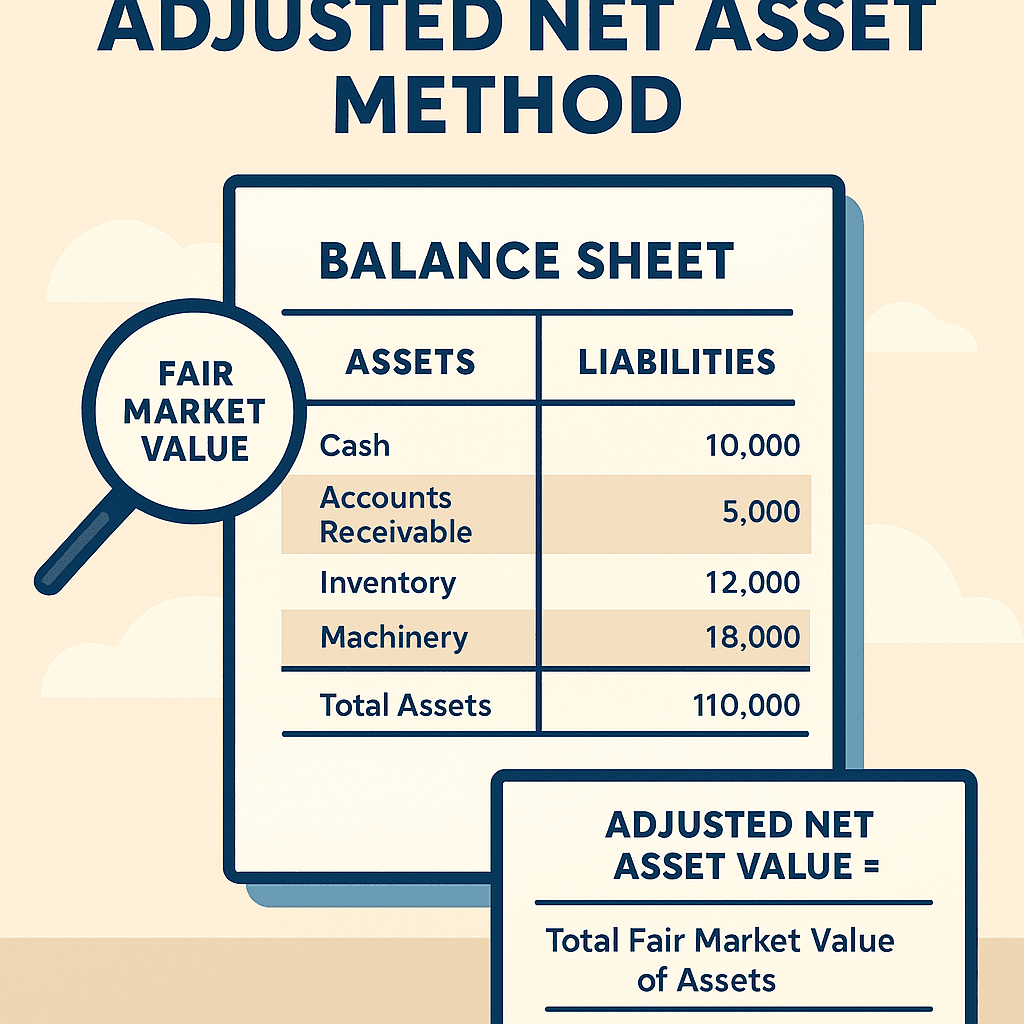

The adjusted net asset method is a valuation technique that takes the traditional net asset value (total assets minus total liabilities) and adjusts the recorded values of the assets to their current fair market values. This provides a more realistic assessment of the business's underlying asset worth, especially when market conditions or the actual condition of the assets have changed significantly since their original purchase.

Think of it like appraising a house you bought years ago. While your initial purchase price is a historical data point, its current value is likely different due to market fluctuations, renovations, and general wear and tear. The adjusted net asset method does something similar for a business's assets.

The Process: Refining the Balance Sheet

Here's a breakdown of the steps involved in the adjusted net asset method:

1. Identify All Assets

This includes the same categories as in the basic asset-based valuation: current assets (cash, accounts receivable, inventory), fixed assets (property, plant, and equipment), and potentially intangible assets (though these are often treated with more scrutiny in this method, as we'll discuss).

2. Determine the Fair Market Value of Each Asset

This is the crucial step where the "adjustment" happens. Instead of relying on book values, you determine the current market value of each significant asset. This might involve:

Appraisals: Hiring qualified professionals to assess the current value of real estate, machinery, or specialized equipment.

Market Research: Comparing the value of similar assets being bought and sold in the current market (e.g., for inventory or vehicles).

Adjusting Book Values: For some assets, like accounts receivable (assessing collectability) or inventory (considering obsolescence), adjustments can be made to their book values to reflect their realizable value.

3. Identify All Liabilities

This step remains the same as in the basic asset-based method. List all the business's obligations to others (accounts payable, loans, accrued expenses, etc.).

4. Calculate the Total Fair Market Value of Assets

Sum up the adjusted fair market values of all the identified assets.

5. Subtract Total Liabilities

Deduct the total liabilities from the total fair market value of assets.

Adjusted Net Asset Value = Total Fair Market Value of Assets - Total Liabilities

This resulting figure is the estimated value of the business based on the current market value of its net assets.

Illustrative Example: "The Old Workshop"

Let's say "The Old Workshop," a small woodworking business, has the following information on its balance sheet:

Asset Breakdown

Asset | Book Value | Estimated Fair Market Value |

|---|---|---|

Cash | $10,000 | $10,000 |

Accounts Receivable | $5,000 | $4,500 |

Inventory (Lumber) | $15,000 | $12,000 |

Machinery (Old) | $30,000 | $18,000 |

Building (Purchased 20 yrs ago) | $50,000 | $150,000 |

Total Assets | $110,000 | $194,500 |

Liability Breakdown

Liability | Amount |

|---|---|

Accounts Payable | $8,000 |

Long-Term Loan | $25,000 |

Total Liabilities | $33,000 |

Book Value Approach:

$110,000 (Total Assets) - $33,000 (Total Liabilities) = $77,000

Adjusted Net Asset Method:

$194,500 (Total Fair Market Value of Assets) - $33,000 (Total Liabilities) = $161,500

As you can see, adjusting the asset values to their current market worth significantly impacts the estimated value of the business, primarily due to the appreciation of the building and the depreciation of the machinery and inventory.

When is the Adjusted Net Asset Method the Right Tool?

This method is particularly useful in the following scenarios:

Asset-Intensive Businesses: Companies with significant tangible assets, such as real estate holding companies, manufacturing firms, or natural resource businesses. The true market value of these assets is crucial.

Companies Where Book Values Don't Reflect Reality: This can happen due to inflation, depreciation, or changes in market demand. For example, real estate purchased decades ago might be significantly undervalued on the books.

Liquidation Scenarios: When a business is being dissolved, the fair market value of its assets is what will ultimately be realized through sale.

Holding Companies: Where the primary value lies in the underlying assets held by the company.

Businesses Not Generating Significant Profits: Similar to the basic asset-based method, if a business isn't currently profitable, the value of its underlying assets becomes a more important indicator of its worth.

When the Adjusted Net Asset Method Might Fall Short

While providing a more accurate snapshot of asset value, this method has limitations:

Ignoring Earning Potential: Like the basic asset-based method, it doesn't directly account for the business's ability to generate future profits, which is a key driver of value for many operating businesses. A highly profitable service business with few physical assets would be significantly undervalued.

Difficulty in Valuing Intangible Assets: While some identifiable intangibles (like patents with a clear market value) might be included, the adjusted net asset method typically doesn't capture the value of goodwill, brand reputation, or customer relationships effectively. These are often the drivers of "excess" earnings.

Cost and Complexity: Obtaining accurate fair market values for all assets can be time-consuming and expensive, requiring professional appraisals.

Not Reflecting "Going Concern" Value: The method values the business based on its individual assets, not as an operating entity with established processes, customer base, and workforce, which contribute to its overall value.

Charting the Appropriateness

Scenario | Adjusted Net Asset Method Appropriateness | Why? |

|---|---|---|

A real estate holding company | High | The primary value lies in the market value of its real estate holdings. |

A struggling manufacturing company with outdated equipment | Moderate to High | Fair market value of assets provides a realistic floor, especially if liquidation is a possibility. Adjustments highlight the actual worth of usable assets. |

A profitable software company with minimal physical assets | Low | The value is primarily driven by its intellectual property, technology, and recurring revenue, which are not fully captured by asset values. |

A retail store with inventory that fluctuates greatly | Moderate | Fair market valuation of inventory at a specific point in time might not reflect average inventory value or potential for future sales. |

A consulting firm with valuable client relationships | Low | The primary value lies in intangible assets (client relationships, expertise) not reflected in the balance sheet. |

The Verdict on Adjusted Net Assets

The adjusted net asset method offers a significant improvement over the basic net asset value by providing a more current and realistic assessment of a business's underlying asset worth. It's a valuable tool, particularly for asset-intensive businesses or when book values are significantly outdated.

However, it's crucial to remember that it primarily focuses on the static value of assets and doesn't fully capture the dynamic potential of an operating business to generate future earnings or the value of its intangible assets. Therefore, like other valuation methods, it's often best used in conjunction with other approaches, especially when valuing profitable and growing businesses where future earnings and intangible value are significant factors. The adjusted net asset value provides a solid foundation, but it's rarely the complete picture.