Comparable Transaction Analysis: Finding Relevant SMB Market Comparables

Here is your SEO-formatted article using proper heading structure:

Gauging Value Through the Rearview Mirror: Understanding Comparable Transaction Analysis for Small Businesses

Imagine you're trying to sell your used car. You wouldn't just pick a price out of thin air. You'd likely look at what similar cars – same make, model, year, mileage, and condition – have recently sold for in your area. The comparable transaction analysis (CTA) method applies this same logic to valuing small businesses.

Instead of looking at balance sheets, earnings projections, or asset values in isolation, CTA focuses on what similar businesses have actually sold for in the recent past. It uses the prices and terms of these past transactions to infer a reasonable value for the business you're analyzing.

How it Works: Finding the Right "Comps"

The core principle of CTA is that similar assets (in this case, businesses) should trade at similar prices. The process involves these key steps:

1. Identifying Comparable Transactions

This is the most critical and often the most challenging step. You need to find data on past sales of businesses that are as similar as possible to the one you're valuing. Key factors to consider when identifying "comps" include:

Industry: The most crucial factor. Businesses in the same or very closely related industries will have similar economic drivers and risk profiles.

Size: Look for businesses with comparable revenue, profitability, and asset size.

Geography: Location can significantly impact value due to local market conditions, customer base, and competition.

Time of Transaction: Recent transactions are generally more relevant as market conditions can change over time.

Transaction Characteristics: Consider the nature of the deal (e.g., strategic acquisition vs. financial buyer, controlling interest vs. minority stake). Controlling interest acquisitions often include a "control premium," making their multiples higher.

Financial Health and Performance: Look for businesses with similar growth rates, profit margins, and overall financial stability.

2. Gathering Transaction Data

Once you've identified a pool of comparable transactions, you need to gather data on their sale prices and relevant financial metrics at the time of the sale. Common data points include:

Transaction Value (Deal Price): The total amount paid for the business.

Revenue (at the time of sale): The business's sales in the period leading up to the transaction (often the last twelve months - LTM).

Earnings (at the time of sale): Various measures of profit, such as EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) or Net Income (after taxes).

3. Calculating Valuation Multiples

Using the transaction data, you calculate valuation multiples for each comparable transaction. Common multiples used include:

Revenue Multiple: Transaction Value / Revenue

EBITDA Multiple: Transaction Value / EBITDA

Net Income Multiple: Transaction Value / Net Income

4. Applying Multiples to the Subject Business

Once you have a set of relevant multiples from the comparable transactions, you apply these multiples to the corresponding financial metrics of the business you are valuing. For example, if comparable businesses sold for an average of 0.8 times their annual revenue, you would multiply your business's annual revenue by 0.8 to get an estimated value.

5. Analyzing and Refining the Results

The application of multiples will likely result in a range of potential values. You need to analyze this range, considering the strengths and weaknesses of each comparable transaction relative to your business. Factors that might warrant a higher or lower multiple for your business compared to the comps include:

Stronger or weaker management team

More or less diversified customer base

Higher or lower growth prospects

Unique assets or liabilities

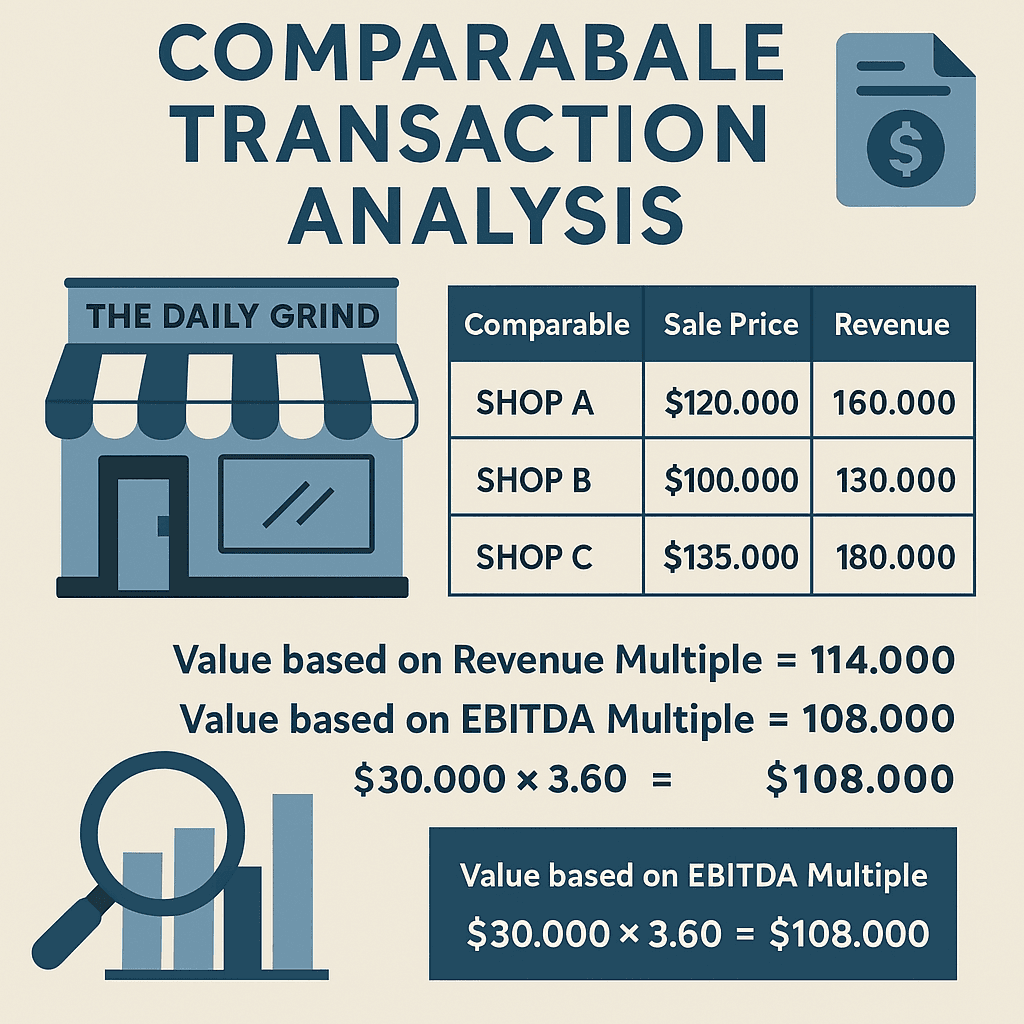

Visualizing the Concept: Comparing Coffee Shops

Let's say you're trying to value "The Daily Grind," a local coffee shop with an annual revenue of $150,000 and an EBITDA of $30,000. You find data on three recently sold coffee shops in similar neighborhoods:

Comparable Coffee Shop | Sale Price | Revenue (at sale) | EBITDA (at sale) | Revenue Multiple | EBITDA Multiple |

|---|---|---|---|---|---|

Shop A | $120,000 | $160,000 | $35,000 | 0.75x | 3.43x |

Shop B | $100,000 | $130,000 | $25,000 | 0.77x | 4.00x |

Shop C | $135,000 | $180,000 | $40,000 | 0.75x | 3.38x |

From this data, the comparable transactions suggest:

Average Revenue Multiple: (0.75 + 0.77 + 0.75) / 3 = 0.76x

Average EBITDA Multiple: (3.43 + 4.00 + 3.38) / 3 = 3.60x

Applying these averages to The Daily Grind:

Value based on Revenue Multiple: $150,000 (Revenue) x 0.76 = $114,000

Value based on EBITDA Multiple: $30,000 (EBITDA) x 3.60 = $108,000

This analysis suggests a potential value range for The Daily Grind between $108,000 and $114,000, based on what similar businesses have recently sold for.

When is Comparable Transaction Analysis a Valuable Tool?

CTA can be particularly useful in the following situations:

Valuing Businesses in Active M&A Markets: When there are frequent transactions of similar businesses, providing ample data for comparison.

Gauging Market Sentiment: Transaction multiples reflect what buyers are actually willing to pay, offering insights into current market conditions and investor appetite.

Providing a Reality Check: It can serve as a useful benchmark to compare against valuations derived from other methods like discounted cash flow or asset-based valuation.

Negotiations for Mergers and Acquisitions: Understanding the multiples paid for comparable deals is crucial for both buyers and sellers in M&A negotiations.

When Comparable Transaction Analysis Might Not Be the Optimal Approach

CTA has limitations and might not be the best method in all circumstances:

Difficulty Finding Truly Comparable Transactions: Every business is unique. Finding perfect "comps" can be challenging, especially for niche businesses or those in less active M&A markets.

Data Availability and Reliability: Information on private company transactions can be scarce and sometimes unreliable. Publicly available data might not provide sufficient detail.

Market Conditions Change Over Time: Historical transaction data might not fully reflect current market dynamics. More recent transactions are generally preferred.

Deal-Specific Factors: Each transaction has its own unique circumstances (e.g., buyer motivations, synergies, urgency of sale) that can influence the price and might not be applicable to the business being valued.

Ignoring Future Potential: CTA primarily looks backward at past transactions and doesn't directly account for the specific future growth prospects or strategic plans of the business being valued.

Control Premiums: If the comparable transactions involved the acquisition of a controlling interest, the multiples might be inflated compared to the value of a minority stake or a business not being acquired for control.

Charting the Appropriateness

Scenario | Comparable Transaction Analysis Appropriateness | Why? |

|---|---|---|

A popular chain of fitness studios in a consolidating market | High | Frequent acquisitions of similar studios provide ample data points for comparison. |

A highly innovative tech startup with no direct competitors | Low | Difficulty in finding comparable transactions with similar technology and growth potential. |

A small, independent bookstore in a rural area | Low to Moderate | Limited number of comparable bookstore sales in the same specific geographic area might make the data less statistically significant. |

A well-established manufacturing company in a stable industry | Moderate to High | If there have been recent acquisitions of similar manufacturing businesses, this method can provide a relevant market-based valuation. |

A business undergoing a distressed sale | Low | Comparable transactions should ideally be "arm's length" and not influenced by duress. Distressed sales often occur at discounted prices. |

The Final Takeaway on Comparable Transaction Analysis

The comparable transaction analysis method offers a valuable, market-driven perspective on small business valuation by looking at what similar businesses have actually sold for. It can be a powerful tool, especially when sufficient and relevant transaction data is available.

However, it's crucial to recognize its limitations, particularly the challenges in finding truly comparable transactions and the fact that past performance is not always indicative of future value. For a well-rounded valuation, CTA is often best used in conjunction with other methods that consider the business's specific financial performance, asset base, and future potential. It provides a crucial "reality check" based on actual market activity.