When to Use SDE vs. EBITDA Multiples in Small Business Valuation

SDE vs. EBITDA: Choosing the Right Metric When Valuing a Small Business

When valuing a small business, understanding its profitability is crucial. Two key metrics often used are Seller's Discretionary Earnings (SDE) and Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). While both aim to represent a business's earning power, they cater to different types and sizes of businesses and have distinct calculations. Knowing when to use SDE versus EBITDA is essential for accurate valuation.

Understanding SDE and EBITDA

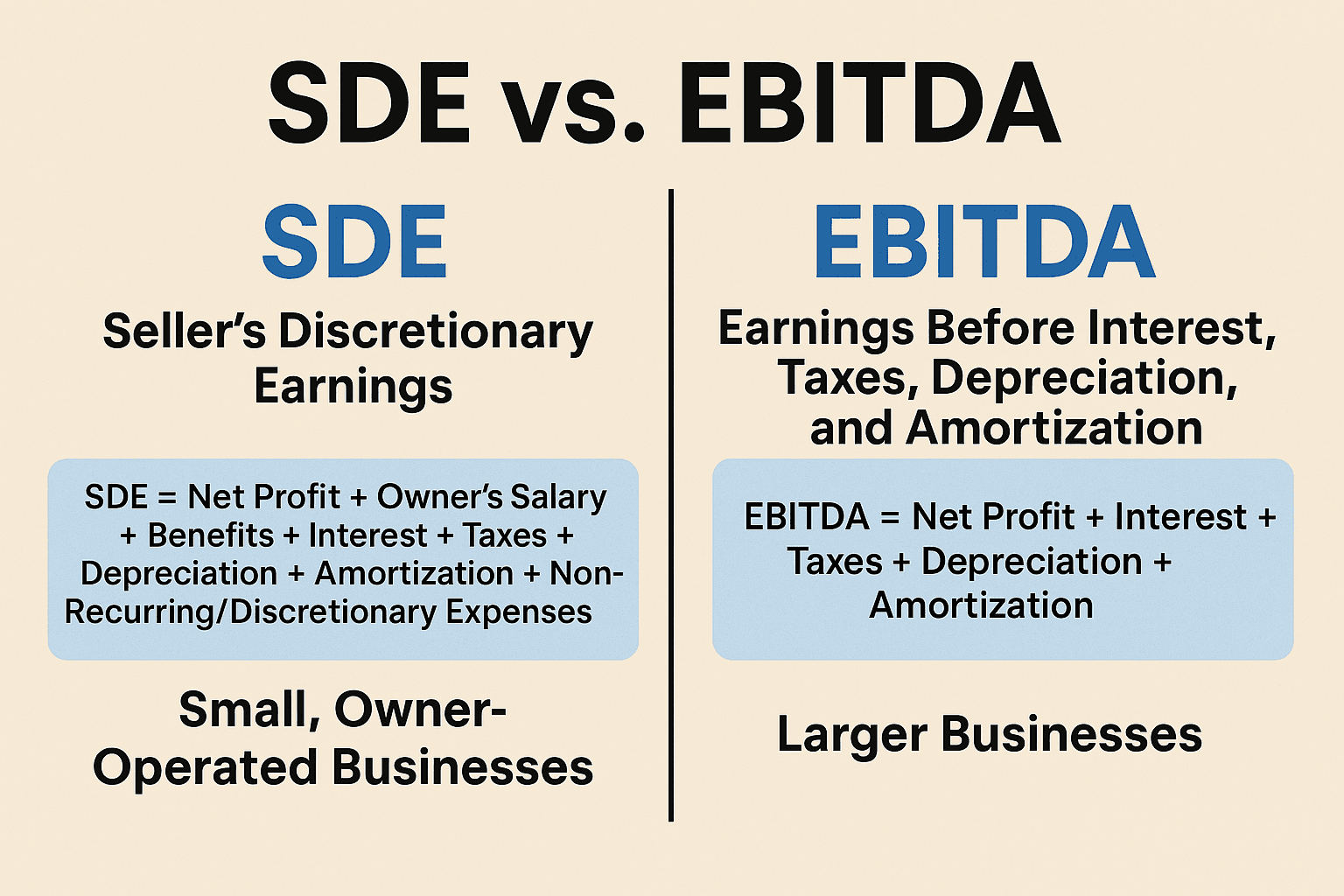

Seller's Discretionary Earnings (SDE)

SDE represents the total financial benefit that a single, full-time owner-operator derives from a business on an annual basis. It's primarily used for valuing small, owner-operated businesses. The calculation typically starts with the net profit and adds back items such as the owner's salary, owner's benefits, non-cash expenses (depreciation and amortization), interest expense, and non-recurring or discretionary expenses that a new owner might not incur. The goal is to show the potential cash flow available to a new owner-operator.

SDE = Net Profit + Owner's Salary + Benefits + Interest + Taxes + Depreciation + Amortization + Non-Recurring/Discretionary Expenses

Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA)

EBITDA is a measure of a company's operating performance. It essentially looks at the profit generated from core operations before the impact of financing (interest), government levies (taxes), and non-cash accounting charges (depreciation and amortization). EBITDA is more commonly used for valuing larger businesses and for comparing the operational profitability of different companies, as it removes the effects of capital structure and accounting policies.

EBITDA = Net Profit + Interest + Taxes + Depreciation + Amortization

When to Use SDE

SDE is generally the preferred metric for valuing:

Small, Owner-Operated Businesses: If the business is heavily reliant on the owner's direct involvement in day-to-day operations, and a likely buyer will also be an owner-operator, SDE provides a clearer picture of the potential income for that buyer.

Businesses with Significant Owner-Specific Expenses: Small business owners often run personal expenses through the business (e.g., personal vehicle, health insurance). SDE adds these back to reflect the true earning power if those discretionary expenses were eliminated by a new owner.

Businesses with Owner Salaries Above or Below Market Rate: SDE allows for the "normalization" of the owner's salary to a market rate, providing a more accurate view of profitability under new ownership.

Businesses with Annual Revenue Typically Under $1 Million (though this isn't a strict rule): Due to the owner-operator focus, SDE is more relevant for smaller entities.

In essence, use SDE when the value to a potential buyer is closely tied to the cash flow they can personally extract from operating the business.

When to Use EBITDA

EBITDA is generally the preferred metric for valuing:

Larger Businesses: For companies with professional management teams in place and where the owner is less involved in daily operations, EBITDA focuses on the operational profitability that would be available to any owner or investor, regardless of their personal involvement.

Businesses with Significant Capital Investments: EBITDA removes the impact of depreciation, which can be substantial for businesses with a lot of fixed assets. This allows for a clearer comparison of operating efficiency.

Comparing Businesses with Different Capital Structures or Tax Situations: By excluding interest and taxes, EBITDA provides a more level playing field for comparing the core profitability of companies with varying levels of debt or operating in different tax jurisdictions.

Businesses with Annual Revenue Typically Over $1 Million (again, not a strict rule): As businesses grow and become less owner-dependent, EBITDA becomes a more standard metric for valuation.

When the Buyer is Likely a Financial Buyer (e.g., Private Equity Group): These buyers often focus on operational cash flow available for debt service and future investment, making EBITDA a key metric.

In essence, use EBITDA when the focus is on the overall operational profitability of the business, independent of ownership structure, financing, and accounting choices.

Vice Versa: When the "Typical" Rule Might Bend

While the above guidelines are generally followed, there can be exceptions:

Small Business with Absentee Ownership: If a small business is already run by a manager and the owner is not actively involved, EBITDA might be a more relevant metric as a buyer wouldn't be factoring in their own owner-operator salary.

Strategic Acquisitions: In some cases, even smaller businesses being acquired by larger entities might be valued using EBITDA if the buyer is integrating the business into their existing structure and the owner-operator model is no longer relevant.

Key Differences Summarized

Feature | SDE | EBITDA |

|---|---|---|

Primary Use | Small, owner-operated businesses | Larger businesses, operational profitability |

Owner's Salary/Benefits | Added back (for owner-operator model) | Not added back (assumes professional mgmt) |

Focus | Cash flow available to a new owner-operator | Operational profitability, independent of capital structure |

Business Size | Typically smaller (under $1M revenue) | Typically larger (over $1M revenue) |

Buyer Type | Often individual owner-operators | Often financial or strategic buyers |

Conclusion

Choosing between SDE and EBITDA depends largely on the size and nature of the business, the role of the owner, and the likely profile of the buyer. SDE provides a "real-world" view of earnings for an owner-operator of a small business, while EBITDA offers a more standardized measure of operational profitability for larger entities. Understanding these nuances is crucial for both sellers looking to accurately value their business and buyers seeking to make informed investment decisions. In some cases, presenting both metrics can provide a more comprehensive understanding of the business's financial health.